Why Your Aging Rolodex is Tanking Your Exit Valuation

TLDR: Your Legacy is a Liability to Private Equity

Let’s cut the fluff. You think your 30 years of handshakes, golf games, and veteran sales reps are an impenetrable moat. To a Private Equity (PE) auditor, they are a massive financial liability.

PE firms do not buy your past; they buy the mathematical predictability of your future. If your revenue is tied to the aging Rolodexes of a few senior reps, you have "Key-Person Risk." When those reps leave, your revenue walks out the door. Because of this, PE will gut your valuation from a premium 7x multiplier down to a 4x multiplier to subsidize their risk.

Furthermore, the buyers have changed. The 55-year-old procurement directors are being replaced by 32-year-old millennial engineers who research silently online, demand frictionless digital assets (like 3D CAD files and ROI calculators), and refuse to sit through your 45-minute discovery calls. If you are invisible to them, your pipeline is already dying.

To defend your exit valuation, you must stop treating marketing as an unquantifiable operating expense (OPEX) and start building a proprietary, digital revenue engine (CapEx).

How Private Equity views your offline sales pipeline, and why capitalizing a digital revenue engine is the only way to protect your EBITDA multiplier.

The Due Diligence Bloodbath

The mahogany table is dead quiet. The operational due diligence is complete. Your engineering tolerances have passed with flying colours. Your balance sheet is clean, and your EBITDA is the healthiest it has been in a decade.

You have spent thirty years building this manufacturing firm from the ground up. As you sit across from the Private Equity (PE) acquisition team, you are mentally calculating your retirement based on a premium 7x or 8x valuation multiplier.

The lead PE auditor, who is a cold, analytical 35-year-old, slides the "Letter of Intent" across the table. You look at the number. It is a 4x multiplier. With a single keystroke, they have just wiped millions of dollars off your life’s work.

You demand to know why.

The auditor doesn’t blink. "Your product is bulletproof," he says. "But your revenue is a flight risk."

Here is the brutal, unspoken reality of modern Mergers & Acquisitions, Private Equity firms buy the mathematical predictability of your future and not your past performance.

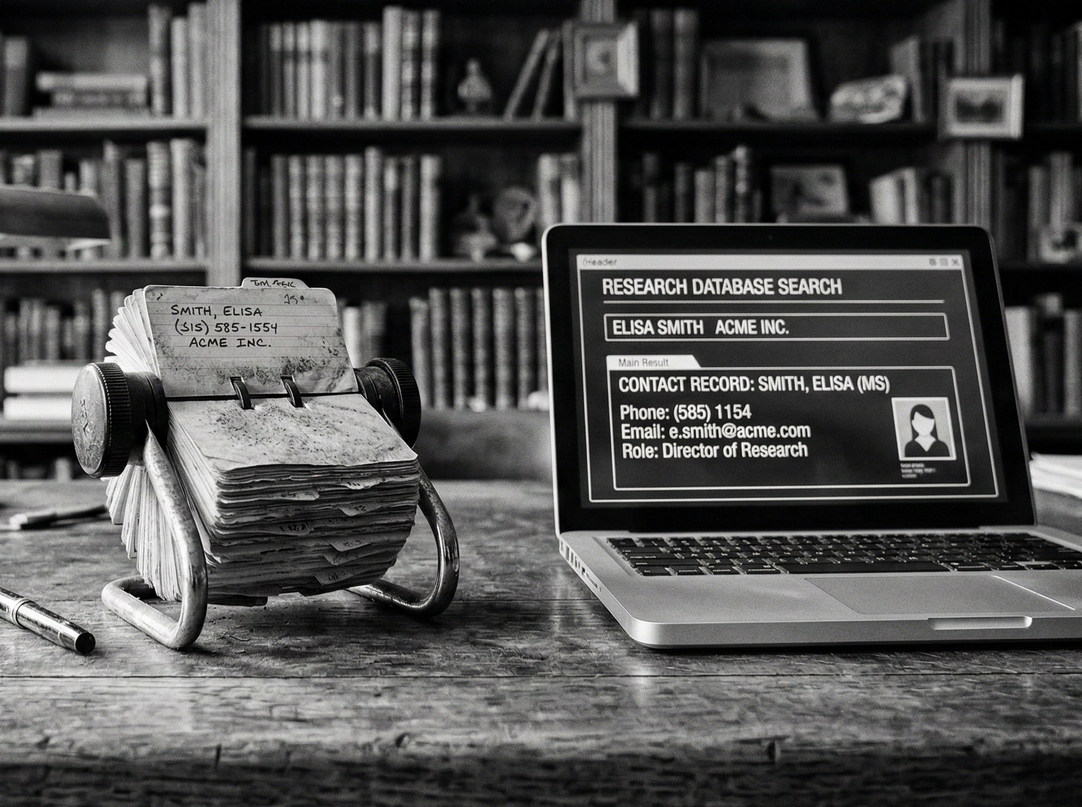

When the auditors looked inside your data room, they saw a company entirely dependent on the aging Rolodexes of three veteran sales reps. They saw a 30-year legacy built on trade-show handshakes, golf course agreements, and offline word-of-mouth.

To you, those lifelong relationships are a point of immense pride. After all, this was how business was done before the internet.

To a Private Equity firm, they represent a massive, unquantifiable liability known as "Key-Person Risk." If your company’s ability to acquire new business is locked inside the heads of men who are five years away from retirement, your revenue walks out the door the day they do. In the eyes of the boardroom, this classifies your company as a highly volatile, depreciating asset.

To secure a premium exit and defend your legacy, CEOs and CFOs must undergo a radical paradigm shift.

You must stop viewing digital marketing as an unquantifiable, monthly OPEX sinkhole outsourced to 24-year-old agency kids. You need to start treating it as a CapEx investment into a proprietary digital asset.

Digitizing your sales pipeline is the only way to mathematically prove your future viability, eliminate key-man risk, and violently defend your EBITDA multiplier at the closing table.

The "Key-Person" Discount (Why Your Rolodex is a Liability)

As a manufacturing CEO, you likely view your offline relationships as an impenetrable moat. You know the purchasing directors at your top five anchor accounts by their first names. Your veteran sales reps have been golfing with the same regional buyers for twenty years. In your mind, this is unshakeable customer loyalty.

In the mind of a Private Equity auditor, this is a ticking time bomb.

When M&A firms conduct revenue due diligence, they apply a ruthless stress test known as "Key-Person Risk." They look at your pipeline and ask the question: If the CEO exits post-acquisition, and if the two senior sales engineers retire in 36 months, does the revenue walk out the door with them?

If your pipeline is bound to personal relationships rather than systemic digital acquisition, the answer is yes. And if the answer is yes, the buyer will not pay a premium for your EBITDA. They will apply a severe "Key-Person Discount" to subsidize the massive risk they are taking on.

This leads directly to the "80/20 Concentration Trap." If 80% of your annual revenue is generated by 20% of your legacy clients which are held together by offline handshakes, you do not have an enterprise system. You have a collection of high-risk friendships. When the PE firm takes over, those personal loyalties do not legally transfer.

What the boardroom is looking to buy is a systematized acquisition engine that functions entirely independent of your veteran staff's charisma. They want mathematical proof that you can acquire new customers in territories where you have zero offline relationships.

If you lack the digitized infrastructure and sophistication to capture modern, out-of-network buyers, the acquiring firm assumes the burden of building that digital acquisitions engine themselves. Of course they will build it, but they will make you pay for it by gutting your exit multiplier.

The Generational Procurement Shift

(The Silent Threat)

If you ask your VP of Sales why close rates are dropping, he will likely blame cheap overseas competitors or a race to the bottom on price. He is wrong. Your veteran reps are not losing the negotiation; they are simply not being invited to the table.

The B2B industrial buyer has fundamentally changed. The 55-year-old procurement director who reliably bought from your team based on a twenty-year offline relationship is retiring.

In his chair sits a 32-year-old millennial engineer.

This new generation of buyers does not want to go to a trade show. They do not want to play golf. Most importantly, they refuse to endure a 45-minute discovery call with a sales rep just to find out if your engineered equipment meets their strict tolerances.

They complete 70% of their vendor research online, in absolute silence, before ever submitting an RFQ.

If your digital presence is essentially an electronic brochure from 2015, you are completely invisible to this buyer.

They are actively searching for frictionless digital assets: downloadable 3D CAD files, interactive ROI calculators, and highly technical spec tear-sheets.

When this 32-year-old engineer cannot find your exact tolerances within three clicks, they do not call your veteran sales rep to ask for them. They simply click over to your competitor’s website.

You are losing seven-figure RFQs to competitors with vastly inferior engineering, simply because their digital delivery mechanism was frictionless.

For the CFO, this demographic shift represents a terrifying financial reality. Your Customer Acquisition Cost (CAC) is skyrocketing because your sales team is relying on outdated, labor-intensive outbound methods that no longer yield results against modern procurement teams.

Private Equity auditors understand this demographic shift perfectly. If they look at your pipeline and see that you have zero digital infrastructure to capture the modern millennial buyer, they immediately calculate the millions of dollars in market share you will bleed to digital-first competitors over the next five years. They will subtract that projected future loss directly from your current exit valuation.

The Financial Shift: From OPEX Sinkhole

to CapEx Asset

If there is one universal truth in the boardroom, it is this: Chief Financial Officers despise traditional marketing. And they are entirely justified in doing so.

For decades, traditional agencies have trained industrial companies to view marketing as a necessary evil—an open-ended Operating Expense (OPEX) that drains the treasury to fund unquantifiable "brand awareness" and "impressions."

Your CFO, hates this because you cannot deposit vanity metrics into a bank account. A traditional marketing retainer is akin to renting a billboard where the moment you stop paying the monthly toll, your visibility drops to zero, and you have no residual enterprise value to show for the capital spent.

To secure a premium exit valuation, the executive team must violently pivot its financial perspective. You must transition your marketing spend from a disposable OPEX sinkhole into a capitalized digital asset (CapEx).

When you build an intent-based SEO architecture, interactive ROI calculators, and frictionless technical spec portals, you are constructing a 24/7 "Silent Sales Engineer." This is proprietary enterprise IP that you own. It works on weekends, it never asks for a commission, and it intercepts the modern 32-year-old procurement engineer at the exact moment of their technical search.

This CapEx reframe fundamentally alters your Customer Acquisition Cost (CAC) trajectory.

With a traditional outbound sales force, your CAC is escalating linearly. Every new deal requires more travel and entertainment expense, more base salaries, and more payroll bloat. Conversely, a capitalized digital revenue engine has a front-loaded build cost, but an exponentially decaying marginal cost. The cost to generate the first inbound RFQ through a custom 3D CAD portal might be significant; the marginal cost to generate the 500th RFQ through that exact same portal is virtually zero.

Over a 36-month horizon, which is the exact window a Private Equity firm audits during due diligence, this digital infrastructure mathematically forces your CAC down while driving your EBITDA margins up.

When M&A auditors look into your data room, they are searching for scalable operational leverage. If they see a company dependent on expensive human capital (sales reps) for 100% of its lead generation, they see a ceiling on profitability. But if they see a digitized, intent-based revenue engine churning out pre-vetted RFQs with a near-zero marginal cost, they now see a highly scalable, capitalized asset.

That is the exact financial mechanism that transforms a baseline 4x multiple into a premium 7x exit.

| The 4x Multiplier (Your Current Flaws) | The 7x Multiplier (What PE Demands) |

|---|---|

| Key-Person Risk: Revenue relies on veteran reps. | Systematized Engine: Revenue is generated by digital assets. |

| OPEX Sinkhole: Marketing is rented "awareness." | CapEx Asset: Marketing is an owned digital infrastructure. |

| Outbound Friction: Phone calls and golf games. | Inbound Frictionless: Self-serve spec portals and CAD downloads. |

| Linear Costs: More sales = more payroll bloat. | Exponential Scale: Near-zero marginal cost for the 500th digital lead. |

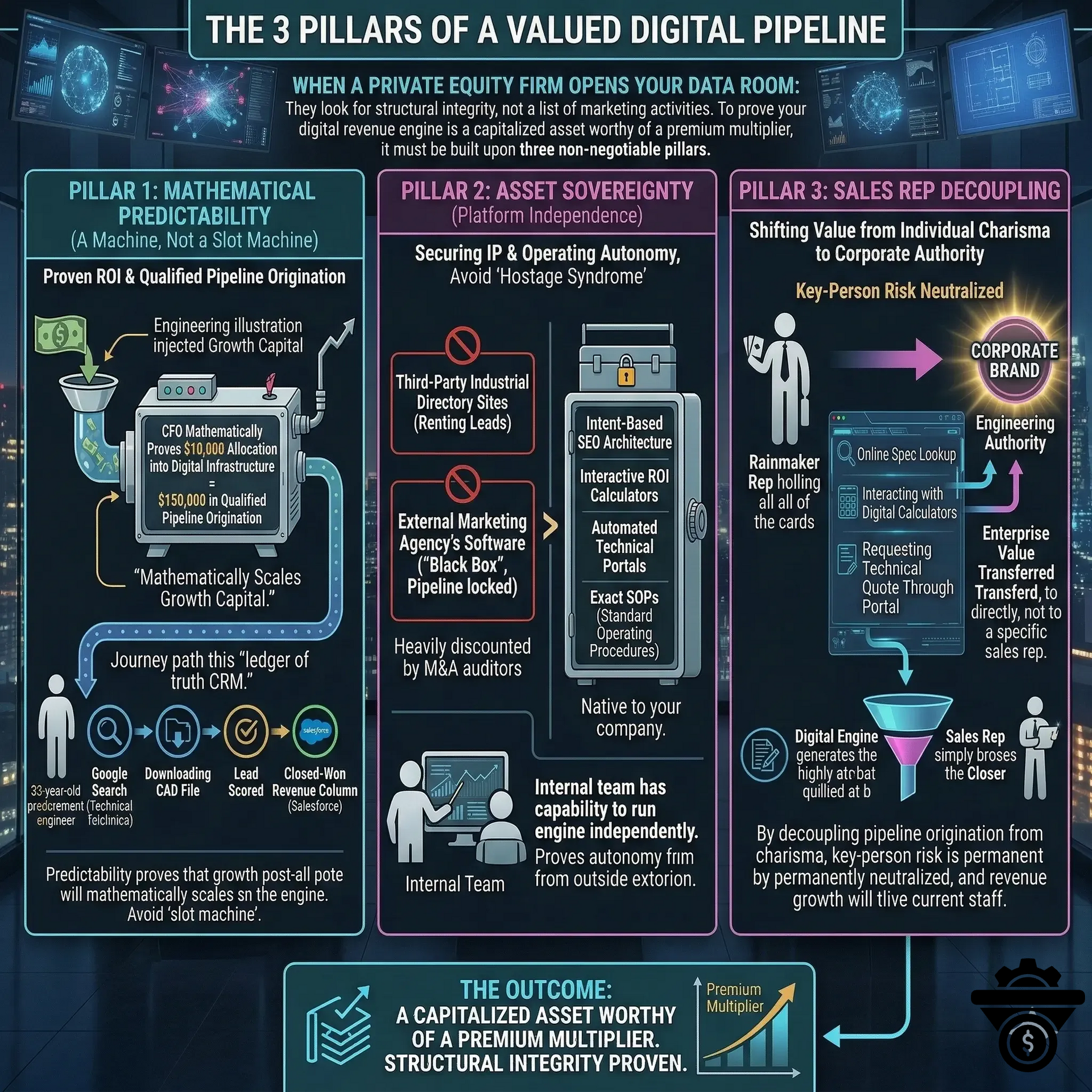

The 3 Pillars to Defend Your Multiplier

If you want a premium exit, you must build a digital infrastructure that proves your revenue is secure. It requires three non-negotiable pillars:

- Mathematical Predictability: You need a clean CRM ledger proving that putting $1X into the digital engine predictably yields $10X in qualified pipeline. PE wants a machine, not a slot machine.

- Asset Sovereignty: You must own the IP, the SEO architecture, and the automated portals. You cannot rent your pipeline from third-party directories or external agencies.

- Sales Rep Decoupling: The digital engine must generate the highly qualified at-bats so the sales rep simply becomes the closer. This transfers enterprise value from the individual employee to the corporate brand, neutralizing your vulnerability to a single "rainmaker."

The Bottom Line: Do not let a 35-year-old auditor discount your life's work because your acquisition model is stuck in the 90s. You need an M&A Digital Readiness Assessment immediately to map the leaks and digitize your pipeline before you sit at the closing table.

The 3 Pillars of a Valued Digital Pipeline

When a Private Equity firm opens your data room, they are looking for structural integrity.

They are not looking for a list of marketing activities which is often believed.

To prove that your digital revenue engine is a capitalized asset worthy of a premium multiplier, it must be built upon three non-negotiable pillars.

Creating all three of these pillars will go a long way in ensuring you maximize your premium to a 7X multiplier.

Missing one of these pillars will be costly because the PE will identify the holes in the "solid company" you think you have spent decades building..

Pillar 1: Mathematical Predictability

A buyer wants a machine, not a slot machine. If your CFO cannot mathematically prove that allocating $10,000 into digital infrastructure yields $150,000 in qualified pipeline origination, the auditor assumes your marketing budget is a slush fund.

Your CRM must be the ultimate ledger of truth. You must be able to track a 32-year-old procurement engineer from the exact moment they searched for a technical tolerance on Google, to the downloading of a CAD file, straight through to the Closed-Won revenue column in Salesforce.

Predictability proves that if the acquiring firm injects growth capital post-sale, the engine will mathematically scale.

Pillar 2: Asset Sovereignty (Platform Independence)

M&A auditors heavily discount companies that suffer from "Hostage Syndrome." If you are renting your leads from third-party industrial directory sites, or if your digital strategy is locked inside the "black box" of an external marketing agency’s proprietary software, you do not own your pipeline.

You are renting it.

To secure your valuation, you must own:

- The IP.

- The intent-based SEO architecture.

- The interactive ROI calculators.

- The automated technical portals.

- The exact Standard Operating Procedures (SOPs)

All of the above must be native to your company. You must prove to the buyer that your internal team has the capability to run the engine independently of outside extortion.

Pillar 3: Sales Rep Decoupling

This is the hardest pill for a legacy CEO to swallow: Your top-performing "rainmaker" sales rep is actually a liability to your enterprise valuation if they hold all the cards.

A valued digital pipeline transfers the enterprise value from the individual employee directly to the corporate brand. When a buyer,

- researches your specs online,

- interacts with your digital calculators, and

- requests a highly technical quote through your portal,

their loyalty is anchored to your company's engineering authority, not to a specific sales rep.

The digital engine generates the highly qualified at-bat. The sales rep simply becomes the closer. By decoupling pipeline origination from human charisma, you permanently neutralize "Key-Person Risk" and prove to the buyer that your revenue growth will outlive your current staff.

The Diagnostic Checkpoint (Your Next Move)

You cannot build a 7x exit multiplier overnight. If you plan to sell your manufacturing firm or seek Private Equity investment within the next 36 months, your digital infrastructure must be built today so it has a proven, multi-year track record of mathematical predictability during due diligence.

The worst financial decision you can make right now is hiring a 24-year-old SEO freelancer or a traditional marketing agency to "refresh your website." That is treating a terminal valuation illness with a cosmetic band-aid.

Before you authorize a single dollar of capital expenditure on digital assets, you must establish objective financial truth.

Your first step is Phase 1: The 30-Day Digital Pipeline Diagnostic.

Think of this not as a marketing audit, but as an M&A Digital Readiness Assessment. Over 30 days, we forensically audit your CRM for revenue leakage, map the exact search terms your competitors are weaponizing against you, and provide the precise architectural blueprint required to digitize your pipeline.

It is a fixed-fee, capped-risk engagement. We identify the leaks. We map the engine. If the math makes sense, we build it.

Do not let thirty years of engineering excellence be discounted by a 35-year-old Private Equity auditor simply because your digital acquisition model is stuck in 1995. Establish the truth today.